So you moved abroad for work, but you still care about what happens with your money back in India. Perhaps it’s for your parents, maybe for your kids’ future education, or you simply want a piece of India’s growth. The problem? You can’t exactly watch the markets every day when you’re dealing with a totally different time zone and your own busy life.

Must Read – NRI Investment Options in India

What Usually Happens with NRI Investment in Indian Markets

Most NRIs I know fall into two camps. Either they don’t invest in India at all because it feels too complicated from far away. Or they make random decisions usually based on some WhatsApp tip from a family & friends or a news headline they happened to catch.

Neither approach really works. The first one means you miss out completely. The second one? Well, that usually means buying when everyone else is excited (prices are high) and panicking to sell when things look scary (prices are low). We’ve all been there.

What Are Multi-Asset Allocation Funds for NRIs?

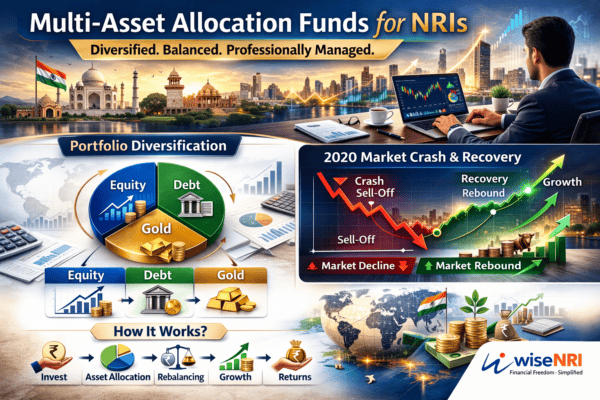

Multi asset allocation funds operate on a flexible investment strategy where fund managers continuously reassess and rebalance the portfolio across equity, debt, REIT and commodities. These asset allocation funds for NRIs adjust based on prevailing market trends, macroeconomic signals, and evolving risk profiles.. When markets are performing strongly, equity weightings tend to increase, whereas periods of uncertainty prompt a defensive shift toward debt instruments and gold.

From a regulatory standpoint, these funds are required to maintain a minimum of three asset classes, with each class receiving no less than 10% of the total portfolio. This structural requirement ensures inherent diversification, offering investors a cushion against market swings while preserving the potential for long-term capital appreciation — an important feature for long-term investment planning for NRIs.

Taxation of Multi-Asset Allocation Funds for NRIs

Funds with 65% or more in equity are treated equity-oriented Multi-Asset Allocation Funds for NRIs, short-term gains (under 12 months) are taxed at 20%, and long-term gains at 12.5% on the amount exceeding ₹1.25 lakh . It is important to note that this ₹1.25 lakh exemption applies specifically to equity-oriented funds.

Funds with below 65% equity attract at slab rates with no indexation benefit, regardless of how long you have held the investment.

For NRIs, the same rules apply with TDS deducted at source — 20% on short-term and 12.5% on long-term equity gains above ₹1.25 lakh. Excess TDS can be reclaimed via return filing.

Benefits of Multi-Asset Allocation Funds for NRIs

- Diversification Across Asset Classes — Spread your investment across equity, debt, and commodities, through Multi-Asset Allocation Funds for NRIs, reducing the impact when any single asset class underperforms and improving overall portfolio diversification for NRIs.

- Professional Rebalancing — Fund managers automatically adjust allocations, boosting equity during favorable periods and shifting toward debt and other commodities during downturns.

- Simplified Investment Management — Gain exposure to multiple asset classes through a single fund, eliminating the need to maintain separate portfolios.

- Tax Efficiency — A single-fund structure streamlines tax reporting compared to managing individual investments across various asset types.

- Emotion-Free Investing — A rule-based system keeps your portfolio on track regardless of market sentiment or short-term noise.

- Long-Term Wealth Building — Designed to ride market cycles and deliver steady compounding growth over extended horizons.

Monthly Investment Options for NRIs

Things NRIs Should Consider Before Investing in Multi-Asset Allocation Funds

Clarify Your Risk Appetite First — Before picking a fund, decide how much volatility you can tolerate and how long you can stay invested.

Sort Your NRI Documentation – FEMA compliance and KYC are non-negotiable. Keep handy with all the necessary documents.

Match the Fund to Your Liquidity Timeline – If you anticipate needing funds within a specific period, choose a scheme that supports your requirement.

Analyse the Fund’s Composition – Study the equity, debt, and commodity split carefully. Review how the fund manager has performed across different market phases, not just during good times.

How Can NRIs Invest in Multi-Asset Allocation Funds?

Here is a quick overview of how to get started with Multi-Asset Allocation Funds for NRIs:

- Open an NRE or NRO Account — You will need either a Non-Resident External (NRE) or NRO bank account with an Indian bank to route your investments.

- Complete Your KYC — Submit the required documents and details.

- Choose a Platform — You can invest directly through an Asset Management Company (AMC) website, a registered mutual fund distributor.

- Select Your Fund and Invest — Once your account and KYC are in place, you can invest as a lump sum or through a Systematic Investment Plan (SIP) in the currency of your NRE or NRO account.

- Repatriation — Investments made through an NRE account allow full repatriation of principal and returns. NRO account investments have repatriation limits as per RBI guidelines, so factor this in based on your needs.

Market Volatility Example: Lessons from the 2020 COVID Crash

Remember March 2020? Markets fell sharply across the board. If all your money was in Indian stocks, you likely saw 30–40% of your portfolio value disappear. That is a painful experience.

People with only fixed deposits did not lose anything but they also completely missed the strong rally that followed.

What about multi-asset funds? They declined too but typically far less sharply than pure equity funds, as the bond and gold portions of the portfolio provided a natural buffer. More importantly, during the crash, these funds automatically rebalanced selling some bonds and buying equities at significantly lower prices. So when markets recovered (and they did, quickly), these funds were well-positioned to capture most of that upside while continuing to earn interest on the bond portion throughout.

Nobody enjoys losing money. But losing less when things go wrong, and being well-positioned when they turn around that is precisely the point.

Bottom Line

Look, I’m not going to tell you these funds will make you rich quick or that you’ll have cool investment stories to share at parties. You won’t.

But what they will do is grow your money along with India’s economy, without you having to stress about it constantly. They handle all the complicated stuff when to buy, when to sell, what to rebalance while you’re focused on your actual life.

If you’re living abroad but want to keep investing in India, this approach just makes sense. Why try to do all this yourself from a different time zone when professionals can handle it automatically?

Something to think about.

This is just information, not financial advice. Talk to a proper advisor before investing.

This post is written by our team member Chetna Sharma.