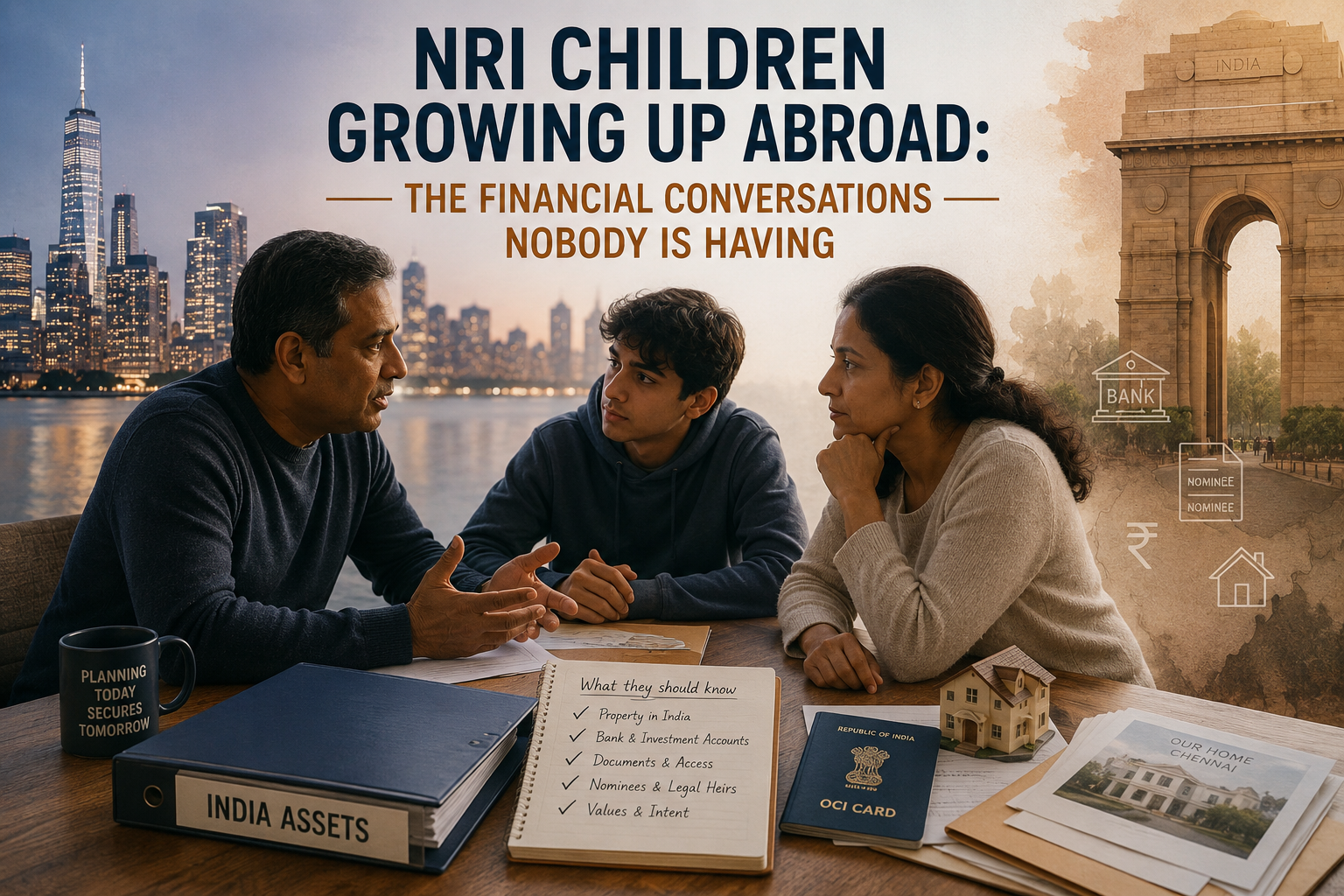

A client of mine, a software engineer in the US, been there 18 years, called me last year about his portfolio rebalancing. Towards the end of the call, he said something that stayed with me.

“My son is 16 now. Born here. He has no idea we have property in Pune. He doesn’t know what an NRE account is. He’s never heard the word FEMA. Honestly, I don’t know how to start that conversation.” He paused. “Or if I should.”

That pause told me more than anything else in that call. Here was a man who had spent fifteen years carefully building assets across two countries, and had never once sat down with his own child to explain any of it. He is not an exception.

Most NRI parents manage the finances. Very few have ever explained them to their children, or to their spouse. When your wealth sits across two legal systems, two currencies, two tax jurisdictions, and two sets of regulations, the cost of that silence is not just emotional. It is financial, legal, and potentially irreversible. The conversations nobody is having are exactly the ones that matter most.

The average NRI household with fifteen or more years abroad has built something genuinely complex. An NRE account here, an NRO account there. A flat in Chennai bought in 2009, still in joint names with an aging parent. Mutual fund folios that have not been KYC-updated since 2017. A PPF account that the spouse nominally knows about. An LIC policy that matures when the NRI turns 58, which is in four years. Nobody in the next generation knows any of this exists.

This is not carelessness. It is the natural result of how NRI families operates.

The earner manages the money. The spouse is involved to varying degrees. The children are kept away from financial complexity partly to protect them, partly because there is never a right moment, and partly because the parent has never quite worked out how to explain an NRO account to someone who has grown up using Venmo. But wealth that nobody else understands is not just disorganized. It is fragile.

What “Growing Up Abroad” Does to Financial Identity

A child born or raised abroad whether in the US, UK, UAE, Singapore, or Australia grows up with a completely different relationship to money than their parents did. Their parents came of age in India. They understand gold as savings. They understand FDs as the sensible thing to do. They have an instinctive feel for how Indian real estate works, what a Power of Attorney means, why a nominee is not the same as a legal heir.

Their children do not have any of this. They have grown up in a world of index funds and ISAs and 401k. India, for many of them, is a place they visit during holidays warm, loud, full of relatives, and entirely separate from their daily financial reality.

This is not a criticism. It is simply a fact about what living abroad does to identity over a generation. And it creates a specific kind of financial vulnerability that most NRI families have not planned for.

When the parent is no longer managing the India assets due to age, illness, or death who steps in? Someone who has never dealt with a sub-registrar office. Someone who does not know the difference between NRE and NRO. Someone who may not even hold an OCI card with current details.

“The most expensive financial mistake an NRI can make is not the wrong investment. It is the undocumented, unexplained asset that nobody can find or access when it matters most.”

The Three Gaps Every NRI Family has but only a few acknowledge them

Gap 1: The Knowledge Gap

Your children do not know what you own. They do not know where it is held, in whose name, what the account numbers are, who the advisor is, or what instructions to follow if something happens to you.

This is the most common gap. And the most dangerous. Indian inheritance and disputes are long and expensive even when documentation is clean. When the documentation is scattered, outdated, or inaccessible to the people who need it, the consequences can follow a family for a decade.

Gap 2: The Identity Gap

A child who grew up in Houston or Dubai may have an OCI card but have they ever used it for a financial purpose? Do they have an Indian PAN card? Do they know how to open an NRO account, submit Form 15CA, or deal with TDS on inherited property? These are not trivial requirements. They are the administrative scaffolding that makes it possible to access Indian assets at all.

Many NRI children discover these requirements for the first time in the worst possible circumstances grieving, jet-lagged, under time pressure, and completely unprepared.

Gap 3: The Values Gap

This one is subtler. But it matters. The NRI parent who built wealth in India did so within a specific cultural and economic context. Property was security. Gold was inherited and not sold. The ancestral home was kept, even if nobody lived there. These were not irrational decisions they were deeply rational ones within the world those parents came from.

Their children may not share those values. Not because they are wrong, but because they grew up in a different world. A financial plan that assumes the next generation will instinctively understand and honor those choices is a plan waiting to unravel.

The Conversation Most NRI Parents Are Avoiding

Ask most NRI parents why they have not had this conversation, and you get a small set of answers.

“They’re too young.”

“It feels morbid.”

“I’ll get to it.”

“They won’t understand.”

The avoidance is human. But the cost of avoidance compounds silently, in the way all financial costs do when left unaddressed.

What the Conversation Actually Needs to Cover

This is not one conversation. It is several, spread over time, adjusted for the age and readiness of the child.

At the foundation level, the child needs to know that India assets exist and roughly what they are. Not a balance sheet just awareness. “We have a flat in Chennai, two mutual fund folios in India, and an NRE account at HDFC.” That alone is more than most NRI children know.

At the practical level, the child needs to know where the documents are. The property papers, the account details, the advisor’s contact, the insurance policies, the will. Not memorised but accessible. A simple folder, physical or digital, that they know exists and can find.

At the regulatory level, the child needs to understand the basics of what being an OCI means financially. That Indian assets may have tax implications. That property cannot simply be transferred abroad without compliance. That a nominee is not automatically the legal heir. These are not complicated concepts when explained properly they only feel overwhelming when encountered for the first time in a crisis.

At the values level, the family needs a conversation about what the India assets actually mean. Is the flat in Chennai an investment to eventually sell? A family home to keep? Something to return to? If that conversation has never happened, you are not leaving behind a plan. You are leaving behind a dispute.

A Practical Starting Point

Most families do not need a formal estate planning exercise to begin. They need a single afternoon and a willingness to start. Write down even roughly what you own in India. The properties, the accounts, the folios, the policies. Who holds them. Who the nominees are. Where the documents are. Who the advisor or CA is. Then share it. With your spouse first, if they are not already fully across it. Then, age-appropriately, with your children. Not as a lecture. Not as a legal briefing. As a conversation about the life you have built, and what you would want for it.

If your children are adults, this conversation is overdue. If they are teenagers, the foundation-level version “this exists, this is roughly what it is” is entirely appropriate.

The Question Worth Sitting With

If something happened to you today your child received a call and was told they needed to manage your India affairs, what would happen next? Would they know who to call? Would they know what exists? Would they have the documents, the account access, the OCI paperwork, the contact for your CA in Chennai?

Or would they spend the next two years learning, from scratch, in the most difficult circumstances, what you could have explained to them over dinner?

My client in the US called me about portfolio rebalancing. He left the call with a different task, sit down with his 16-year-old this weekend. Not to explain FEMA. Just to say, “We have a flat in Pune“, here is roughly what it means, and one day it will matter that you know.

This article is written by our Team member Manika Dhanetwal.