A client in Dubai called me last month. He is 51, runs a logistics business, and last year he parked a large sum in an NRE fixed deposit at a rate he was very happy with. Good rate. Indian bank. Fully repatriable. On paper, a smart move.

Then he opened his statement and went quiet. The rupee had slipped from the low 80s toward 95 against the dollar. In dollar terms, the money he had “grown” at 7 percent had barely moved. “Hemant,” he said, “I earned the interest and the currency ate it. What was the point?”

He is not alone. Almost every NRI who chases a high rupee rate eventually meets the same ghost: rupee depreciation. You win on the interest line and quietly lose it back on the exchange line.

To be fair to him, this past year was not a normal one. Over the long run the rupee tends to slip around 4 percent a year against the dollar, a slow and fairly predictable drag you can plan around. This year the fall was far steeper, driven largely by the conflict in the Middle East and the oil shock that came with it. He was not careless. He was caught by an exceptional year.

So when the RBI did something unusual with FCNR deposits on 8 June 2026, his question is exactly the one worth answering.

You earned the interest. The currency ate it. That is the NRI’s oldest, quietest loss.

What RBI Actually Announced

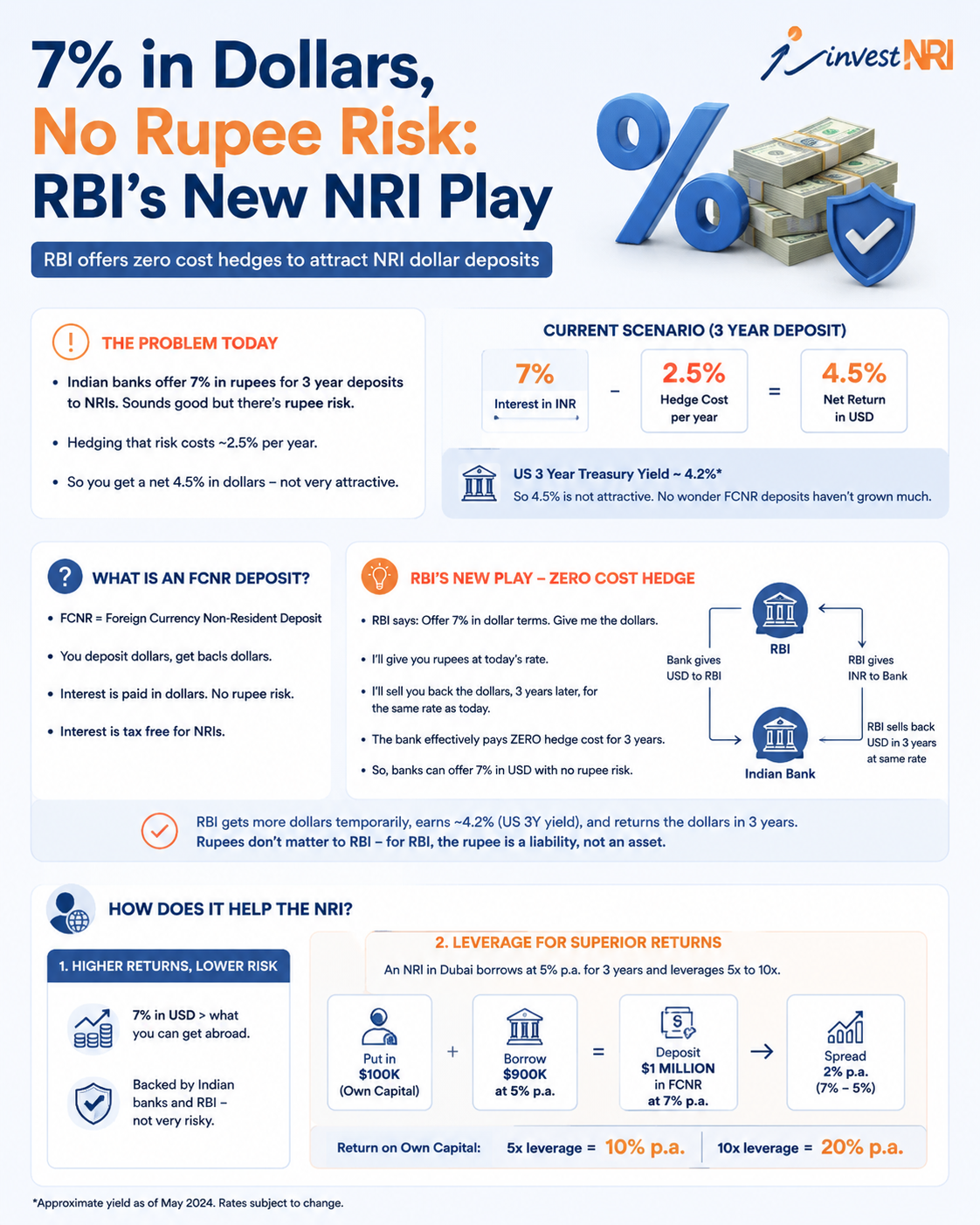

On 8 June 2026, following the Governor’s statement of 5 June, the RBI opened a US Dollar to Rupee swap facility for fresh FCNR (B) deposits of three to five year tenor.

In plain language: the RBI takes the dollars off the bank’s hands, gives the bank rupees today, and agrees to sell those same dollars back to the bank at the same rate three years later. The bank’s single biggest headache with a dollar deposit just disappeared. And that headache has a name. The hedge cost.

Why FCNR Deposits were not exciting

An FCNR deposit is dollars in, dollars out. You hand over dollars, you get back dollars, the interest is paid in dollars. No rupee risk for you. Lovely in theory.

The problem sits with the bank. It cannot do much with dollars inside India, so it converts them to rupees to lend. To return your dollars three years later, it has to buy those dollars back at a future rate nobody knows today. Covering that uncertainty costs the bank roughly 2.5 percent a year.

So the math used to look like this. The bank earns its rupee rate, loses about 2.5 percent to hedging, and offers you maybe 4.5 percent in dollars. With three year US treasuries yielding around 4.2 percent, why would any NRI lock money for three years to earn 0.3 percent more? They would not. So FCNR money stayed away.

Why Is RBI Doing This Now?

Step back and ask why the RBI would hand banks a free hedge. The answer is in the numbers. FCNR (B) inflows have all but dried up. In FY26 they collapsed by 86 percent, to around 946 million dollars, from about 7.1 billion dollars the year before. The dollars India was quietly relying on simply stopped coming.

At the same time the rupee has been under steady pressure, brushing record lows near 95 to the dollar. India would like more stable dollars in the system to steady the currency, and it would rather get them without raising domestic interest rates and cooling the economy. A swap window does exactly that.

We have a template for this. In 2013, during the taper tantrum, the RBI ran almost the same play and pulled in roughly 34 billion dollars in a matter of months, about 26 billion of it through FCNR deposits, which helped steady a falling rupee. This is that playbook, dusted off for 2026. Banks are already estimating 35 to 50 billion dollars could flow in this time.

The RBI needs these dollars urgently. You do not. That difference is the whole game.

Here is the part worth holding on to. The urgency, the September deadline, the push to make this attractive, all of it is the system’s need, not yours. A sovereign in a hurry is not a reason for you to be in one. Let the offer earn its place in your plan on its own merits, not because someone in Mumbai is in a rush.

How the Zero-Cost Hedge Changes the Math

Now the RBI carries that currency leg itself. The bank pays close to nothing to hedge the principal. Which means it can pass the full rupee rate, roughly 7 percent, straight through to you in dollar terms.

Read that again slowly. Seven percent. In dollars. From an Indian bank deposit. With the rupee risk on your principal carried by the RBI, not by you.

7 percent in dollars, with the principal’s rupee risk parked with the RBI. That has not been on the table for years.

Banks have moved fast. HDFC Bank has already lifted its FCNR (B) dollar rate to 6 percent for three to five year deposits, a jump of more than two percentage points, and other large banks are clustering around the same level. A few smaller banks are pushing closer to 7 percent. So read 7 percent as the top of the range for now, with 6 percent the more common number from the big names. Compare the actual rate, tenor and bank before you decide.

What This Means for You as an NRI

Strip away the jargon and here is what an NRI actually gets:

- Around 7 percent in dollar terms, which beats most equivalent dollar deposits available abroad today.

- FCNR interest is tax-free in India for NRIs. Your country of residence may still tax it, so check that.

- It is backed by an Indian bank, and behind the bank sits the RBI swap.

- You give dollars and you get back dollars. The exchange line stops eating your interest line.

This is the deposit my Dubai client wishes he had opened a year ago. Same 7 percent, but no currency ghost waiting in his statement.

The Tax Question: What an NRI Actually Pays

This is where FCNR quietly beats almost every rupee deposit. Interest is fully exempt from Indian income tax for NRIs under Section 10(15)(iv)(fa) of the Income Tax Act, and there is no TDS. But “tax-free” has edges worth knowing, and they depend entirely on where you stand. Three situations cover most people.

1. You hold to maturity as an NRI. The interest is completely tax-free in India, no TDS, and the principal is fully repatriable. You should still report it as exempt income in your Indian return if you file one, but nothing is payable here. The only catch is abroad: your country of residence may still tax the interest. A US person is taxed on worldwide income, while a UAE resident typically is not. Any relief usually runs through the relevant tax treaty.

2. You withdraw early. Pull out before one year and FCNR rules pay no interest at all, so there is nothing to tax. Withdraw after a year but before maturity and you get interest for the period held, usually at a lower rate, and the bank may apply a penalty. Whatever interest you do receive stays tax-free in India as long as you are still an NRI when it is paid. Leaving early does not change the Indian tax position.

3. You return to India during the term. You can run the deposit to maturity, you simply cannot open fresh FCNR deposits or renew once you are a resident. Tax then follows your residential status. While you are an NRI or RNOR, which for many returning Indians covers the first couple of years back, the interest stays exempt. Once you become Resident and Ordinarily Resident, interest accruing from that date is taxable as income from other sources at your slab rate. Interest earned while you were still NRI or RNOR stays exempt. Many returning NRIs move the money into an RFC account to keep it in dollars, though RFC interest becomes taxable once you are a full resident.

FCNR is tax-free in India only while you are. The day you become a full resident, the clock starts.

The 2026 swap scheme changes the rate, not the tax rules. And because the answer turns on your exact residency timeline and your home country’s treaty with India, this is one to confirm with a CA for your own situation before you commit.

The 2013 Echo, and the Leverage Temptation

We have seen this film before. In the 2013 FCNR window, when the rupee was under heavy pressure, the RBI ran a similar scheme. A lot of NRIs did not just deposit. They borrowed abroad and geared up.

The arithmetic is seductive. Put in 100,000 dollars of your own, borrow another 900,000 dollars abroad at say 5 percent, and place the full 1 million dollars in a 7 percent FCNR deposit. That is a 2 percent spread on money that is mostly borrowed, which can translate into a 10 to 20 percent return on your own capital. This time too, the RBI has effectively said leverage is fine.

Now the part the brochure will not stress. Leverage cuts both ways. Your 5 percent borrowing cost may be floating, not fixed. A 2 percent spread is thin, and it only survives if your cost of borrowing stays put for three full years. A margin call abroad does not care about your three year plan in India.

“Risk is what is left over when you think you have thought of everything.” – Morgan Housel, The Psychology of Money

The Fine Print Most People Skip

A clean deposit is genuinely attractive here. But read the boundaries before you wire money:

- There is a one year lock-in on the underlying deposit. Banks may allow premature exit after that at their discretion, but the swap with the RBI itself cannot be cancelled.

- The RBI swaps back the principal, not the interest. So a small residual rupee risk sits on the interest portion. That mostly sits with the bank, but it is the reason the rate is not pure free money.

- Your deposit carries bank credit risk. Deposit insurance covers only about Rs 5 lakh equivalent. The rest is exposure to that bank’s health.

- Tax-free in India does not mean tax-free everywhere. A US person, for instance, is taxed on worldwide income.

The Real Risk Is Not the Rupee

Here is the uncomfortable bit. Everyone debating this scheme is arguing about the currency. But for the principal, the currency risk is already handled. So that is not where people will get hurt.

The real risk is behavioural. It is the pull to turn a safe, sensible dollar deposit into a leveraged bet because the spread looks easy and a neighbour in the same building is doing it. In 25 years of advising families, the losses I have seen rarely came from a bad product. They came from a good product used badly. It is not a numbers game. It is a mind game.

What to Do, and By When

The window is real and it is dated. Deposits that qualify for the swap must be mobilised by 30 September 2026, and the facility stays open up to 16 October 2026. It came into effect immediately.

A few practical notes. The best rates tend to come early, before banks fill their books, so waiting rarely helps unless you expect rates to rise. Each bank can also tap the RBI swap only once a week, against deposits raised the prior week, so very late money can hit processing queues. If you are even thinking about leverage, model the downside first, not the upside. And if the rupee picture matters to your plan, our note on the best time to send money to India is worth a read alongside this.

If you want the longer history of how banks have wrapped FCNR with currency contracts in the past, and where the tax grey areas sit, see our older piece on FCNR deposits with forward cover.

My Dubai client is doing the unglamorous thing this time. No 10x gearing, no spreadsheet heroics. Just a clean FCNR deposit, dollars in and dollars out, sleeping at night while his money earns.

After a year of watching the rupee quietly undo his returns, that peace is worth more to him than any spread. Sometimes the smartest NRI move is not the cleverest one. It is the one that lets you stop checking the exchange rate every single morning.

Frequently Asked Questions

What is the RBI FCNR swap facility of June 2026?

It is a US Dollar to Rupee swap the RBI offers banks on fresh FCNR (B) deposits of three to five year tenor. The RBI absorbs the bank’s hedging cost on the principal, which lets banks offer NRIs a much higher dollar rate than before.

How much can an NRI earn on an FCNR deposit now?

Large banks have moved to around 6 percent in dollar terms for three to five years (HDFC Bank, for example, is at 6 percent), and a few smaller banks are pushing close to 7 percent. The exact rate depends on the bank and the tenor, so compare before you commit.

Is FCNR interest tax-free for NRIs?

FCNR interest is exempt from tax in India for NRIs under Section 10(15)(iv)(fa), with no TDS. Your country of residence may still tax it, so check your local rules or speak to a tax professional.

Is FCNR interest still tax-free if I return to India?

It stays exempt while you are an NRI or RNOR, which often covers the first couple of years after returning. Once you become Resident and Ordinarily Resident, interest accruing after that date becomes taxable at your slab rate, while interest earned earlier stays exempt.

What is the last date to invest?

Deposits must be mobilised by 30 September 2026 to qualify for the swap, and the facility remains open up to 16 October 2026. There is a one year lock-in on the deposit.

Thinking about whether this fits your plan?

An FCNR deposit at 7 percent in dollars is attractive, but the right answer still depends on your wider picture: your currency needs, your time horizon, your existing India exposure, and whether leverage has any place in your situation. That is the conversation we have with NRI families every week. Talk to the WiseNRI team and we will help you decide whether to use this window, and how much of it.