Are you an NRI looking to build or maintain a good credit score? With the ever-evolving credit system and stringent policies, navigating the credit landscape can be overwhelming. But fear not, as we’ve got you covered! In this guide, we’ll walk you through everything you need to know to establish a solid credit history.

So, let’s get started on your journey towards financial stability and success.

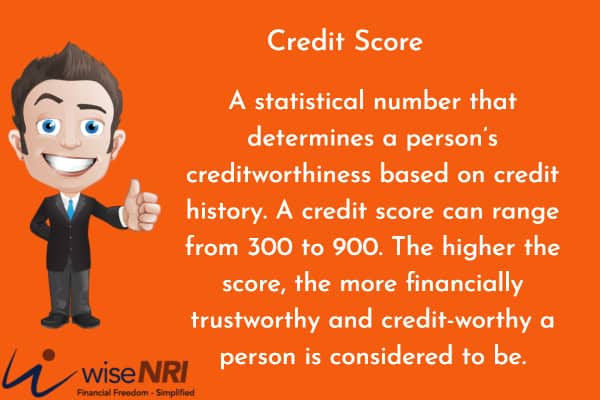

Credit Score

A statistical number that determines a person’s creditworthiness based on credit history. A credit score can range from 300 to 900. The higher the score, the more financially trustworthy and credit-worthy a person is considered to be.

Must Read- Financial Tools For NRIs

Just like you would be wary of lending money to a stranger as you do not know if you will get the money back, banks and NBFCs would want some assurance of the creditworthiness of a borrower before they lend money. A credit score comes into play here as it uses financial parameters to arrive at an individual’s creditworthiness.

As an NRI, maintaining a good credit score is beneficial. You have a better chance of getting a loan (e.g., a home loan). You can get a credit card approved quickly. You will have more negotiation power to get a loan on better terms (e.g., lower interest rate) or a higher limit on the credit card or a more feature-rich credit card.

Check – Personal Loan For NRIs

Who Calculates the Credit Score?

Transunion CIBIL, Experian, Equifax, and CRIF High Mark are the four major credit bureaus that can determine your credit score. Your credit score with each of them might vary as –

- They have different scoring models

- Banks and financial organizations may not report all your financial activities to all the bureaus.

But all the credit bureaus use the same factors to arrive at the credit score.

Must Read – NRI Checklist

How is the Credit Score Calculated?

The credit score is calculated considering four factors with weightage assigned to each of them –

- Repayment History- Making repayments on time is the foundation of good credit standing. Make regular repayments for your loans and credit card dues. Even a single late payment can drag down the score by about 100 points. If you have financial issues, inform your lender in advance about the delay in repayment. If it is a rare occurrence, they may allow the exception.

- Age of credit – The length of your credit history is a key factor. The longer the tenure of your loan, the older your credit card, the better your score can be, as it implies you have been paying installments and dues regularly. A longer-term loan with prompt payments is considered better than short-term loans as it shows financial responsibility.

- The number of credit accounts – Secured loans include home loans, car loans for NRIs, etc. Unsecured loans are personal loans, credit cards, etc. The more the proportion of unsecured loans, the more you might be seen as a risky borrower. The higher the proportion of secured loans, the higher your credit score can go. Ensure that you have a healthy mix of unsecured loans and secured loans.

- Credit Utilization Ratio (CUR) – Credit utilization refers to the amount of credit that you use vis-à-vis the amount if credit you have. A lower credit utilization will have a positive impact on the credit score. For example, the more you use your credit card, the higher the CUR, and the lower the credit score can go.

- The number of credit enquiries – Every time you enquire for a loan or a credit card or apply for refinancing a loan, the lender will run a credit check. It implies that you borrow too much hurting your credit score.

Must Read – NRI Credit Cards

How NRIs can Build a Good Credit Score?

NRIs can build a good credit score by

- Ensuring that you have some credit accounts

- Servicing your credit accounts properly with timely payments and appropriate utilization.

- Keeping the right balance of secured and unsecured credit

How can NRIs maintain a Good Credit Score?

Since the credit score is not a constant number, it is critical that you follow some measures to maintain the credit score at a high level –

- Experts recommend to maintaining the Credit Utilization Ratio within 30%. Request a higher limit on your existing credit card or look for a different credit card if you regularly exceed this ratio.

- Do not request or apply for loans, credit cards, and other credit products too often. You can always get information on new products, features, etc., from the Internet, your financial advisor, or banking relationship manager. Request a higher limit on your existing credit card or look for a different credit card if you regularly exceed this ratio.

- Friends and relatives might ask you to be a guarantor for loans. It is easy to get swayed by emotions and relationships. But if they default in payment, your financials can be affected, and your credit score will also drop. Therefore, be a guarantor only for creditworthy parties.

- Check your credit score regularly so that you are aware of your current score and can correct discrepancies if any. One of our clients had taken a personal loan 10 years ago, but due to a misunderstanding, the loan remains unpaid to this day. Although he has not taken out any loans since then, his credit score is now poor, and he was recently denied a car loan. Despite earning a good income, his past credit history has come back to haunt him.

- You might have credit cards issued in India that you may not use much as you live abroad. Sometimes it is better to keep these cards active as an extended credit history indicates you are prompt in paying off your dues.

Read – NRI Home Loans In India

Are credit scores transferable between countries?

Credit scores are not usually transferable between countries. This affects your access to financial products when you live in a foreign country or return to India. You will have to build a credit history in the country of residence, and if you think you will have a lot of financial activity in India, you will have to build a credit score in India as well.

It is crucial to have good credit standing. It leads to better opportunities in personal finance matters, which is essential for success and peace of mind in life.

By following the tips and strategies outlined in this guide, you can improve your creditworthiness and increase your chances of accessing credit facilities in India. Remember, building and maintaining a good credit score requires patience, discipline, and consistency. Start today, and enjoy the benefits of a strong credit history for years to come.

Please share any unique or unconventional strategies you’ve discovered to boost your credit score in the comment section.

Can you help me to get my credit check in India? I left India 6 years ago and I lost my mobile number which was linked with my bank account. Is there any way to get a credit check report without mobile number?

How can I check credit score of mine, I’m NRI Stay in US for 10 yrs now

How can I check credit score of mine, I’m NRI Stay in US for 10 yrs now

I am an NRI, I have good credit score in UAE, but I don’t have a good credit score in India. Does it affect my Home loan request?

Iam a NRI How to find cibil score

Credit score required for NRI to apply home loan

How to check credit score

How to get CIBIL report for NRI

What is my cibil score? I’m an NRI with no transactions in India for more than 13 years