I am working in the US what should I do with my 401k plan before moving back to India or can we withdraw 401k from India? These are very common question considering the number of non-resident Indians that are working in the USA. Today we are going to answer these.

NRIs working in the USA participate in one of the retirement plans commonly known as 401k plans. The 401(k) is a qualified retirement plan with deferred tax benefits under US tax laws. NRI employees can invest a part of their salary in the 401(k) account, however, the employer may or may not match your contribution.

In This Article :

- Types of 401(k) Retirement Accounts

- 401k withdrawal from India

- What is Traditional IRA

- What is 401k in India

- NRI Should Know 401k before moving to India

Types of 401k Retirement Accounts

Among the six different 401(k) retirement plans and a 403(b) plan, NRIs can opt among the following three types –401(k), Traditional IRA, and Roth IRA/401(k).

401k in India

If your employer offers the defined contribution 401(k) plan, then they are matching your contributions to your corpus. Contributions are made before taxes and therefore the entire sum is taxable at withdrawal at prevailing rates.

Because of the matching contribution from the employer, a 401k in India is offering the best way to quickly save for your retirement. The investment options are also limited to those offered by the employer.

Check – Why Should NRIs Save for early retirement

Traditional IRA

A self-sustained retirement plan, an IRA has only your contributions. You can open a new IRA account or when you leave your job then you can rollover your 401(k) Plan into one. You can decide your investment options – aggressive or conservative. Here also, contributions are made from pre-tax income, and the tax is deferred until withdrawals.

Roth IRA/401k Plans

Investments in Roth IRA are made from post-tax income, making withdrawals (of principal) tax-free. Any earnings, however, are taxable at prevailing rates. Early withdrawals do not attract taxes or penalties as investments were made post-tax. Earnings also become tax-free if you hold the account for more than five years or have turned 59½.

Which plan should you opt for?

As the 401(k) plans significant tax benefits and a matching contribution from the employer, if you are eligible, they do go for it.

For others, if post-retirement you expect to be in a lower tax bracket, then opt Traditional IRA otherwise Roth IRA is a better choice. Usually, salaried people would be in the lower tax bracket at the time of their retirement, thus we suggest opting for Traditional IRA for them. For business persons, and high-flying professionals like physicians, attorneys, Roth IRA is suitable.

Similarly, if you don’t think that you will be in the USA till the time you retire and would come back to India then again Roth IRA is a better choice.

Check – Why NRI Invest In India?

What to do with the 401k plan before moving back to India?

If you have invested in the 401(k) India or the Traditional IRA, then moving back to India before you turn 59½ may attract penalties and tax liabilities on the entire corpus.

You must opt between if you are going to cash out, leave the fund as it is, or rollover to another account.

Let’s discuss each of them here one by one.

Leave your 401(k) Plan as it is

If you choose to not do anything your employer will continue to manage it without any contributions. You would be able to defer taxes and earn tax-free growth till you turn 59½.

One downside is that if your employer decides to pull out of the fund, you will have no option but to either cash out or rollover to an IRA. It means you will have to keep in touch with your employer, even after you are back in India, which can be an issue for many.

Must Read – Planning for Retirement In India – 5 Easy steps NRI Can use

Rollover to an IRA

By rolling over your 401k plan to an IRA you can lower your tax liability and need not pay the 10% penalty as you are still invested in a qualified account and not withdrawing.

A penalty of 10% will apply if you withdraw from this account before 59½ years of age. But certain exceptions apply for emergency and big-ticket expenses. These include out-of-pocket medical expenses, buying your first home, permanent disability, and qualified higher-education expenses (including tuition, books, supplies, room, and board) at eligible institutions.

One problem with opening an IRA is that many companies do not cater to non-US addresses, so get clarity on this aspect before opening the IRA. Another concern is that when you turn 70, you must compulsorily start withdrawing under the Required Minimum Distributions requirements.

You can also transfer your IRA fund to a retirement fund in your home country, but you will have to pay taxes in the USA on the withdrawal. As India has DTAA with the USA, you can claim tax credit here while filing IT return based on the taxes paid in the US. India US tax treaty 401k is part of it.

Check – 10 Best NRIs Investments options in India 2022 – High return plans

Rollover to a Roth IRA

The investment made in the Roth IRA account is from post-tax dollars, so it is less complicated. At the time of withdrawal, contributions are tax-free, only the earnings are taxed at the prevailing rates.

While moving back to India, if you fall are in a lower tax slab, then you can consider a roll-over to Roth IRA. You will pay taxes on the amount you are rolling over, but all subsequent withdrawals would be tax-free in the USA. As RMD does not apply to Roth IRA, you can continue to save even after you turn 70 for purposes like children’s higher education, or their seed money.

Must Read – Pension plan for NRIs In India – Dream retirement

401k Withdrawal from India

If you cash out your 401(k) before you are 59½ or permanently disabled, then a 10% early withdrawal penalty is applicable over and above the appliable tax, in the case of 401(k) and Traditional IRA.

If your children are staying longer in the USA, then making them designated beneficiaries would make later withdrawals tax-free.

If there is a need to cash out, then wait for the next tax year, if you can. As you would have no US income in that year and fall in a lower tax bracket. The 10% penalty would still apply if you were younger than 59½.

In general, if you plan to come back to India sooner than later, then Roth IRA accounts are the best bet considering lesser tax hassles and offering liquidity.

Budget 2021-22 Return to India 401k Issue

Budget 2021 promised to address the double taxation issue by taking into account the specific needs of NRIs. An example of this is income from retirement accounts opened outside of India. It is common for NRIs working in the US to invest in 401(k) accounts to take advantage of tax benefits. (Or people working in Singapore investing in CPF or in UK Qrops)

Workers working temporarily in the US and later returning to India faced different tax laws in both countries. Returning home as residents of India, they paid taxes on their worldwide income, which is on an accrual basis. And since the source of such income (in this case, the retirement account) comes from the US, it also became taxable in the US under US tax laws, regardless of whether or not residing in the US.

In addition, there is the issue of different tax periods for the respective countries. NRIs usually pay taxes on the same retirement income with no tax credits in India and the US, albeit in different years. Personal taxes, Payable on a calendar year basis in the USA, Germany or Singapore, and on a fiscal year basis in India.

First of all, check if your country of residence has a DTAA with India. Earlier there were doubts as to whether such recurring NRIs would receive tax relief for such taxes paid in India under the Double Taxation Agreement (DTAA). This will likely be resolved soon by the government.

India US Tax Treaty 401k India Double taxation and the fight for it is clear for NRIs and the Ministry of Finance of India has made commendable efforts to improve this in the 2021-22 Union budget. Earlier, there were several tax-related issues in India that plagued NRIs and caused problems.

Some of these were: Non-compliance in the taxability period in India and the USA.

“To address this, the Union Budget 2021-22 proposed adding a new Section 89A to the Act to ensure that the income a particular person derives from a particular account is taxed in the manner and yearly prescribed by the crediting of the Central Government Challenge.

Funds for taxes paid abroad in India are taxed on a receipt basis in the USA and on an accrual basis in India”

Check – Tax Strategies for NRIs

FAQs – Can I withdraw 401k from india

Q: What is a 401(k) plan?

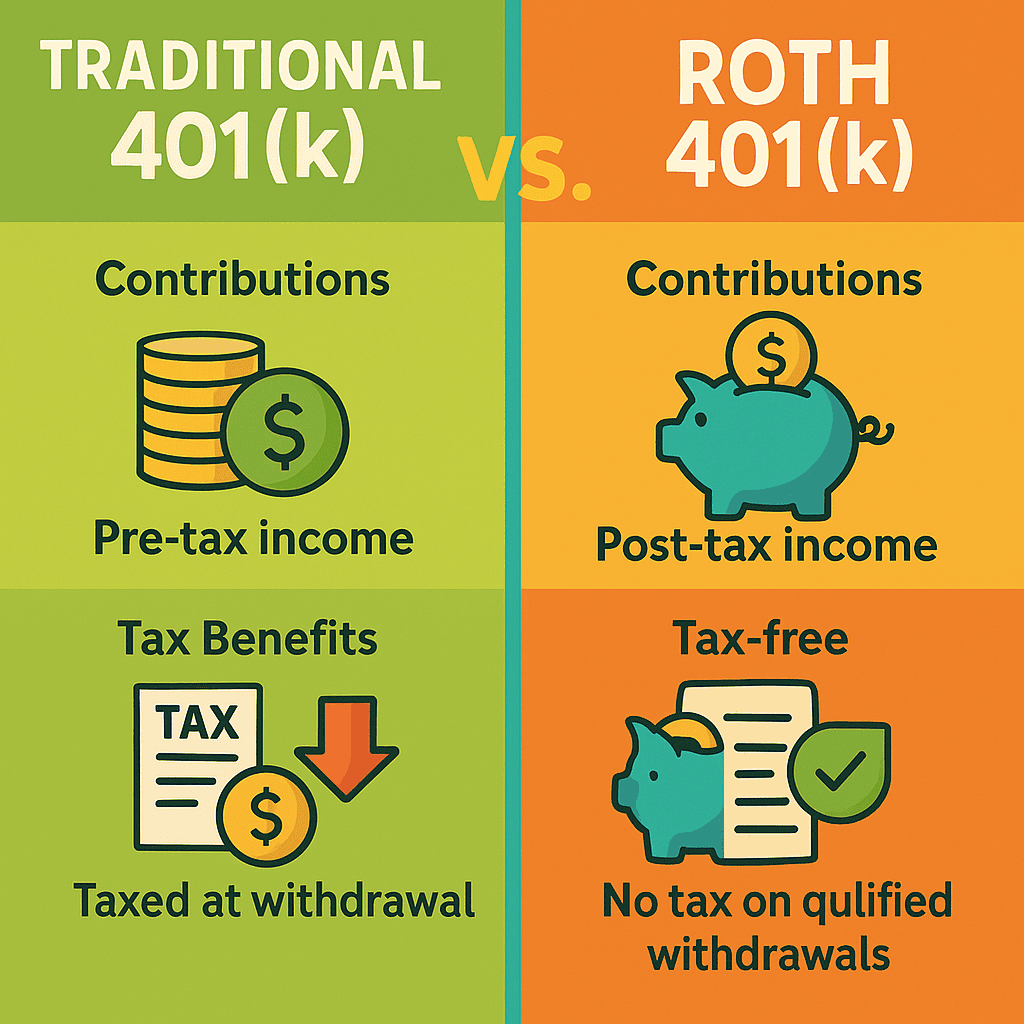

A: The 401(k) plan is a workplace-based retirement savings plan that allows an individual to make annual contributions and invest with the aim of building a corpus for post-retirement. Employers can contribute to the plan. There are two basic types:

- Traditional 401(k) – In this plan, taxes on employee contributions and any earnings from the investment are deferred until withdrawal.

- Roth 401(k) – In this plan, income tax is paid immediately on the earnings that the employee deducts from each paycheck and deposits into the account. Income earned on the account, such as interest, dividends, or capital gains, is tax-free. Withdrawals made after retirement are tax-free.

Q: Can an NRI withdraw funds from their 401(k)?

A: NRIs can withdraw funds from their 401(k) accounts. However, tax implications and potential penalties are associated with early withdrawals (before the age of 59½) or if the account is in operation for less than five years.

Q: What are the tax implications for 401(k) withdrawals by NRIs in the USA?

A: When an NRI makes an early withdrawal from their 401(k), the withdrawal is subject to income tax rules in the USA.

Participants in a traditional or Roth 401(k) plan are not allowed to withdraw funds until they reach age 59½ or become permanently unable to work due to disability. If these conditions are not satisfied the withdrawal is considered an early withdrawal and is subject to a 10% penalty. The entire 401(k) withdrawal will be taxed as income in the USA, even if the person has returned to India when they withdraw the funds.

Q: How can NRIs who become resident Indians manage tax on for 401(k) withdrawals effectively in India?

A: The lumpsum withdrawal amount would be taxed in the USA. The NRI, who is now a resident Indian, will then have to file their tax returns in India in which they can declare the 401k withdrawal proceeds and claim a credit on the taxes paid in the US.

Due to different taxation rules, there can be a mismatch in claiming foreign tax credit because tax liability arises in India when the income accrues. In contrast, the USA taxes it upon withdrawal or redemption of the retirement funds.

Guide – Personal Finance for US NRIs

Q: How 2021 budget changed 401k Withdrwal?

Effective from fiscal year 2021-22, a provision in the Income Tax Act allows the deferral of taxation in India on accrued income from eligible retirement funds to the year of withdrawal and enables claiming foreign tax credit in India in that year, subject to specified conditions. NRIs can exercise this option using Form 10EE, which needs to be filed electronically before the due date for filing tax returns. It is applicable for the year in which it was filed and for all subsequent years unless the individual becomes an NRI again. This provision is also extended to resident Indians who have been NRIs in Canada and U.K.

Monthly pensions are taxed only in India for NRIs from the USA who have returned to India as per provisions of DTAA (social security benefits and public pensions not included). NRIs need to submit the necessary documentation in the USA so that tax is not withheld. Social security benefits are taxable in the USA and exempt from income tax in India.

The tax implications of 401(k) withdrawals for NRIs and returning NRIs are complex. Getting guidance from a financial planner with expertise in taxation planning based on the laws in India and the USA can help you optimize your tax outgo on your retirement savings.

Now you know what are the options that you have before moving back to India 401k. If you have any questions regarding 401k moving to India add them in the comments. If you have experience related to how to withdraw from 401k in India – must share it in the comment section.

I want to withdraw my 401-k amount, please let me know the process!

How to withdraw 401k amount if I don’t have any USA bank account. I am resident of India right now.

Hey Asha,

If you don’t have a U.S. bank account and are a resident of India, you can still withdraw your 401(k) funds by contacting your 401(k) provider. They may allow wire transfers to an Indian bank account, though some providers may require a U.S. bank account. Ensure to provide your Indian account details and comply with the required documentation, including tax forms. You may also face tax withholding and penalties for early withdrawal if under 59½.

“I want to withdraw my 401k as I returned back to India long back

and need funds”

How to withdraw 401k amount if I don’t have any USA bank account? I am resident of India right now.

I have a 401k account in USA and returned on 29th December so if I withdraw money now what is the taxes I need to pay??

Hi Vashnavi,

If you withdraw your 401(k) now, you may pay 20–30% in U.S. taxes and a 10% early withdrawal penalty if you’re under 59½, plus possible Indian taxes.

Hi

I have few questions on 401k. I am listing them below

1>In 401K I invest 3%in PRE-TAX and 2% in ROTH. Now will I face any issue to rollover 401K amount to traditional IRA?

2> In case of my death before withdrawing 401K amount, how can my spouse or son get the access of the amount from India?

3>Do I need leave any saving account open in USA to withdraw 401k amount from India or if I leave open one saving account in USA will it help me to withdraw 401k amount after or before the age of 59 1/2?

Hey Kaushik,

1. You can roll over pre-tax 401(k) to a Traditional IRA;

Roth 401(k) must go to a Roth IRA.

2. Name a beneficiary; they can claim funds from India

via U.S. bank.

3. Keep a U.S. bank account open.

What do I need to do to make hassle free withdrawals of 401k from India?

Hey Vikrant Gupta

To make hassle-free 401(k) withdrawals from India, keep a U.S. bank account open, update your address with the plan provider, name beneficiaries, use U.S. tax filing services, and consider working with a CPA familiar with expat retirement distributions.

Can I withdraw my 401k once I back to India before 59 Years of age?

Hey Sourabh Gujjar,

Yes, you can withdraw your 401(k) after moving to India before age 59, but you’ll incur a 10% early withdrawal penalty and owe U.S. income tax. Some exceptions apply; consult a tax advisor to explore penalty-free options.

I was in H1b visa till 2018 and moved to India from USA. While coming I closed my bank account and mobile number is discontinued. I am with same employer and like to know how to claim the amount.

Hii Sampath Kumar,

Contact your 401(k) plan provider via email or employer’s HR. Update your contact info, request distribution or rollover forms, and provide Indian bank details if allowed. A U.S. bank account helps, but isn’t always required for claiming funds.

“Need help in filling w8ben for doing 401k withdrawals..

What needs to be filled in line 10”

Hello Peyush Kumar

On Line 10 of Form W-8BEN, describe the income type you’re withdrawing, like “Pension and annuity payments from U.S. retirement accounts.” If claiming treaty benefits, include the treaty article number, e.g., “Pension income under Article [number] of the U.S.-[Country] Tax Treaty.” Ensure accuracy and consult a tax professional if needed.

401k withdrawal consultation

How to withdraw from 401 k while being in india

Hey Sachit,

Reach out to the administrator of your 401k plan. This is usually the HR department of your former employer or a designated plan administrator. Inform them of your change in employment status and your intention to manage your 401k account.

How to withdraw 401K amount while I am not active participant , as I moved to Indian payroll

Hi Suriyadeepan,

Reach out to the administrator of your 401k plan. This is usually the HR department of your former employer or a designated plan administrator. Inform them of your change in employment status and your intention to manage your 401k account.

I need help in filling up W8 BEN Form, Part III and Line 10. I am planning to withdraw from 401K as I repatriated to India in 2018

Hi Venkata,

Check the box for Line 10, indicating that you are claiming special rates and conditions under a tax treaty between the U.S. and India. Next, consult the tax treaty between the U.S. and India to determine the applicable tax rate for your specific situation. Tax treaty rates can vary depending on the type of income and the taxpayer’s status.

I want to withdraw from 401K. I am in India now

Hi Bharat,

First of all, Review the rules and regulations of your specific 401k plan. After that, Get in touch with the administrator of your 401k plan to inquire about the withdrawal process. They can provide you with the necessary forms and guidance.

I have a rollover IRA in the US and I am a Canadian citizen, OCI and ROR Ordinarily Resident in India for over 20 years. I will be 59 1/2 in about six months.

All IRA funds are in Money Market Fund so I receive monthly dividends on it. Every year, I have been showing the total dividend income in India in “income from Other Sources” and paying normal tax on it as per my tax bracket. This year, the online ITR 3 form is asking for more information such as “DTAA of Dividend”.

There was no tax paid in the rollover IRA, so I am not sure in which ITR schedule I should enter that information. Could you please help out?

The exact error message I am getting during validation is “Dividend income must be equal to 1a(i) of Schedule OS – DTAA of Dividend – System calculated value of interest expenditure u/s 57(i)] of Schedule OS. This error message is displayed five times. When I click on any of those, it takes me to Schedule OS Line10, 2.

Hey Shyam,

Based on the error message you provided, it seems that the issue is related to dividend income and interest expenditure while using Form ITR (Income Tax Return) and Schedule OS (Other Sources) in India.So, You should enter the dividend income from the rollover IRA in Schedule OS, under the appropriate section for DTAA (Double Taxation Avoidance Agreement) of Dividend. The error message indicates that the dividend income should be equal to 1a(i) of Schedule OS, and the system calculates the interest expenditure under Section 57(i). Make sure you accurately input the dividend income and any relevant details to resolve the validation error.

I am 40 years old. I have money in 401 K that I will either keep in 401 K or roll over to IRA.

Question: After I reach 60 years and start withdrawing 1) How much can I withdraw each month without incurring a penalty; 2) What is the tax that I need to pay on the gains? My understanding is that as a non resident alien, my tax bracket is 30% and there are no tax brackets for non resident aliens.

Hey Phssyk one,

After reaching 60 years, you can withdraw from your IRA or 401(k) penalty-free under the IRS rule of “Substantially Equal Periodic Payments” (SEPP) or by reaching the age of 59½. The tax on gains during withdrawal will depend on your tax residency at the time of withdrawal. If you are a non-resident alien, the tax rate on gains will typically be 30% unless a tax treaty between the US and your home country specifies a different rate.

Hi Manita, Considering the same situation here – what will be the tax situation if the home country is India.

After age 59 1/2, there is no penalty. You can withdraw as much as you want.

The tax you will pay will based on your total income and your jncome tax bracket. If you withdraw, $1,000 it will be added to your total income for the year and you just file your regular income tax return.

Due to the treaty between India and the US, upon withdrawal, your plan administrator will withhold 30% tax. You will have to show this in your income tax return. You will get the withheld tax back. You won’t get all of it because you still have to pay tax in India.

How to withdraw 401k to INR

Hello Team D,

Start with Contact your 401(k) plan administrator to initiate the withdrawal process. After that the funds will be distributed to you, and you will receive them in USD.

Now, you can then transfer the USD to your Indian bank account through a wire transfer or other suitable means.

Once the funds are in your Indian account, your bank or a remittance service can help you convert the USD to INR at the prevailing exchange rate.

Nominee getting 401k savings in my death

401k funds options while moving back to India

Hey Karan,

You have three options: You can keep the fund in the 401(k) account even after leaving the US.

Or you can rollover the 401(k) funds to an Individual Retirement Account (IRA) in the US, which can provide more control over investment options.And lastly it is also depending on Indian regulations and your new employment, you might be able to transfer the funds to a qualifying Indian retirement account, such as the National Pension System (NPS) or a recognized pension plan in India.

Hi Manpriya, Can the 401k amount be transfered to NPS (National Pension Scheme) in India once I move back from US, do share more information on this front.

I am an Indian citizen and worked in USA on a H-1B work visa from age 24 to 30 year old. I opened a ROTH ira (after tax dollars) and contributed in it to buy mutual funds and Stocks/ETF’s. I returned back to India forever at age 30 and kept the money in ROTH ira as it is. I am planning to withdraw money from this ROTH ira by selling stocks/ETFs and mutual funds after I become 60 years old. ROTH withdrawals are tax free in USA after 59&1/2. But will I need to pay taxes in India for those withdrawals? Also will I need to file taxes in USA as well? Also can my ROTH account company pay me withdrawal in Indian bank or will I need to have a US bank account too? Please note that when I return to India at age 30 I will no longer have a US address and no US bank account. What will be my tax situation in this case and what do I need to do?

Hey Sujay,

1. Roth IRA withdrawals are generally not taxable in India, as they are considered post-tax contributions. Consult with a tax advisor for specific guidance based on India’s tax laws at the time of withdrawal.2. As a non-resident alien, you won’t have to file US tax returns for Roth IRA withdrawals, as they are tax-free for qualified distributions.3.Check with your Roth IRA account provider if they can facilitate withdrawals to an Indian bank account. Some may allow international transfers, but it’s essential to verify their policies.4.Not having a US address or bank account shouldn’t impact your Roth IRA withdrawals. It’s essential to maintain communication with the account provider and update your contact details as needed.5.Roth IRA withdrawals should generally be tax-free in both the USA and India. However, tax laws may change over time.

I worked in US and had a 401K plan , now two year back , I moved back to India. How can get my money back from 401k account with lower tax rate.

Hello Parag

As an NRI who previously worked in the US and had a 401(k) plan, you have a few options for withdrawing your funds and minimizing your tax liability. Here are some possible strategies to consider:

1.Leave the money in the 401(k) plan: If you have a balance of less than $5,000, your former employer may require you to withdraw the funds, but if you have more than that, you may be able to leave the money in the plan. This can be a good option if you plan to return to the US at some point, as it allows you to continue deferring taxes on the funds. However, if you keep the money in the plan and later withdraw it, you will be subject to US income tax and possibly state tax as well.

2.Withdraw the funds and pay US taxes: If you decide to withdraw the funds from the 401(k) plan, you will be subject to US income tax on the distribution. The tax rate will depend on your overall income and tax bracket, but it’s important to note that the distribution will be taxed as ordinary income, which means it may be subject to a higher tax rate than other types of income, such as capital gains or dividends. You may also be subject to an early withdrawal penalty of 10% if you are under age 59 1/2.

3.Roll over the funds into an IRA: Another option is to roll over the 401(k) funds into an individual retirement account (IRA). This can be a good option if you want more control over your investments and lower fees than you may have had in the 401(k) plan. If you do a direct rollover from the 401(k) to the IRA, you can avoid immediate taxation on the distribution, but you will still owe US income tax when you eventually withdraw the funds from the IRA.

4.Consider a partial or phased withdrawal: Depending on your financial situation, you may be able to withdraw the funds over a period of time rather than all at once. This can help you avoid a large tax bill in any one year and may allow you to take advantage of lower tax rates in India. However, it’s important to consider the potential impact on your retirement savings and the fees and penalties associated with multiple withdrawals.

Hi Arjun,

Can you please explain more and clarify on what you meant by this sentence – “it’s important to consider the potential impact on your retirement savings and the fees and penalties associated with multiple withdrawals”.

I need to withdraw my 401k before retirement..i moved back to India in 2019..

If you need to withdraw your 401(k) before retirement, you will be subject to US income tax and possibly state tax as well. Here are some steps you can take:

1.Contact your former employer’s 401(k) plan administrator: They can provide you with the necessary paperwork to start the withdrawal process. Keep in mind that the process may take several weeks to complete.

2.Consider the tax implications: When you withdraw the funds from your 401(k) account, you will be subject to US income tax on the distribution. The tax rate will depend on your overall income and tax bracket. You may also be subject to an early withdrawal penalty of 10% if you are under age 59 1/2.

3.Plan for potential currency conversion costs: If you withdraw the funds and want to transfer them to India, you may need to convert the funds into Indian rupees. Keep in mind that this can come with additional fees and costs.

4.Consult with a tax professional: To minimize your tax liability and ensure you are complying with US tax laws, it is advisable to consult with a tax professional who is familiar with cross-border tax issues.

I have moved back to Indian in June 2022. My 401K account is with my employer in US, not converted to IRA.1. What will be better option – keep account with employer or move to IRA?2. I want to close my US bank account as I don’t want to maintain minimum balance. Do we need US bank account if I decide to withdraw 401?

Hello Praveen

1.Whether it is better to keep your 401(k) account with your employer or move it to an IRA will depend on your individual circumstances, including your investment goals and preferences, fees and expenses associated with each option, and the investment options available in each account. It may be beneficial to consult with a financial advisor or tax professional who can help you evaluate your options and make an informed decision.

2.You do not necessarily need a US bank account to withdraw funds from your 401(k) account. However, you will need to provide the account information for the bank or financial institution where you would like the funds to be deposited. Keep in mind that you may incur additional fees or costs for transferring funds internationally or converting currency.

I moved back to India in late 2022. Can i still contribute to my US traditional IRA account?

Hi Sagar,

No.

I need help for 401k withdraw form India

does roth 401(k) distributions attract tax in india if i move back to india after my age 60 years?

Hi Ourangeswarag,

if you move back to India after age 60 and become a tax resident in India, the tax treatment of your Roth 401(k) distributions will depend on the tax laws and regulations in India.

you should consult with a qualified tax professional who can provide you with advice based on your specific circumstances and the current tax laws in India.

I want to connect with you on this matter. Can you please reach me on email. thanks.

Hi Manish,

we will get in touch with you.

Can I change traditional 401k to IRA at ROR status in India

is it goo to invest in 401 k m going to shift in US for 3 yrs aft that i will be back to my country

Yes. Company match and tax savings helps you make more money in your 401K.

If we withdraw 401k from india howmuch tax we have to pay.Also where we need to pay the tax in India or US

I wanted to withdraw my 401k as IAm in delhi i want this to dposit in indian bank directly what info i should give them

I am in US now on H1B and will be moving to India next year. I am planning to withdraw my 401K after reaching India next year. What will be the tax implications? I understand there is a 10% penalty in US and applicable taxes. Also, if I withdraw only 25K an year, will that be taxable?

I have returned to India for good after being in USA for nearly 7 years this April. I’m 31 years old and want guidance in managing my bank a/c, 401(k) , Simple IRA and brokerage accounts. Can you help me?

401k withdrawal from India

How do i withdraw my 401k?

Hi Asha,

You need to consult with a local advisor in USA.

If I withdraw 401k before age 59 and I am Indian citizen how much taxes USA will withhold if my income is zero in USA and I am non resident alien

Hi Ashish,

You have to pay 10% penalty if you withdraw 401k before the age of 59.

Hi Ashish,

Your pre tax contributions to 401k is basically tax deferred income stored for retirement. So at the time of withdrawal, 401k withdrawals are added to your global income for that financial year and taxed. On top of this please add on the 10% penalty on the absolute value being withdrawn from 401k.

Hi I am in India and want to withdraw my 401K funds(USA). My doubt here is, as i don’t have a resident address in USA, does it attract any other extra taxes for using my Indian address as resident address?

Other problem is getting spouse intent notarized. Can this notary be done at USA consulates in India?

Hi Satish,

Kindly consult with your CA

I am citizen of USA from INDIA. I am getting pension in India from my previous employer every month. how to get it in USA?

Hi Ganapatbhai,

You can transfer it to NRO to USA saving account

I would like to know tax rates for 401K or IRA accounts after coming to India? I am on VISA currently, no Greencard

Hi ,

As per my knowledge No, you don’t need to pay tax on 401K in India.

how can i transfer 401k funds to indian bank account?

Hi Sosenderma,

To transfer money from a 401(k) to a bank account, you should send a withdrawal request to the 401(k) plan administrator. It can take up to seven business days for the withdrawal to be processed, and you can expect to receive your funds shortly thereafter.

I travelled to USA for a project deputation and stay got extended. Due to pandemic and visa extension issues, could not travel back to India and open NRI account

Hi Lithikau

An NRO (current/ savings) account can be opened by a foreign national of non-Indian origin visiting India.

There are many banks now that can open NRE account online.

Need to know what I should do to transfer my 401k from US to India with least tax implications.I have returned to India now

Hi Reuben,

By rolling over your 401k plan to an IRA you can lower your tax liability and need not pay the 10% penalty as you are still invested in a qualified account and not withdrawing.

A penalty of 10% will apply if you withdraw from this account before 59½ years of age

Hi, I am taking out money from my IRA 401K account and need to fill out W8BEN form. There is line 10 in Part-II where we need to mention Special rates and conditions from the INDIA-USA tax treaty, any idea on that?

Hi Saurabh

Kindly consult your CA regarding this.

I’ve returned back to India in 2006, but I have not withdrew my 401k investment yet. Do I have to pay taxes in the US/ India if I do a lumpsum withdrawal?

Hi Kishore

Yes. Lumpsum withdrawal will fall under the purview of taxation in the US and India.

Will 401k gains be taxed in india as worldwide income even when no distributions is taken from the 401k aacount on a yearly basis

Hi Sunny

No, you don’t need to pay tax on 401K in India.

Took U.S 401(k) lumpsum withdrawal from India ( being in ROR status ). Will both 401(k) account’s contributions and appreciations be taxable in India ?

Hi Ranjan,

The taxes are paid upon withdrawal on the entire amount (contributions plus the earnings). Premature withdrawal attracts tax along with a 10% penalty.

Hi, moved back to india 3 years ago, have a 401k account still in US (stayed in us for 7 years) now question is do I have to declare that in my India ITR, if yes how?

Hi Navam ,

you do not need to declare that in India ITR.

I have been a resident of India for 13 years and I am a US citizen. I have a 401k account in the US – in which I have invested in specific US stocks and held on to them.

If I trade in the 401k – sell stocks that have made gains BUT do not withdraw from the 401k until I am 59.5 years of age – do the gains that I realize IN The 401k attract tax in India?

No, the gains in the 401k do not attract tax in India. However, Once you withdraw all of the amount you have to use DTAA method to show the income and file in India.

I have my 401k still in US

Is it advisable to leave the 401k in ROTH IRA and cash out after 59 1/2 years ? What would be tax implication in India ?

Assume I became India resident by staying for 365 days in a year. I have my IRA account in USA. At this point, I start to withdraw from my IRA. US will tax me. Let us say that is 22%.

I have to pay tax on that in India too because I became resident. My rate is India will be easily 30%. Will I get 22% credit, because I paid tax to USA?

According to the article in Union budget you will get the credit in India. But speak to a CA before filing your returns.

Should I go through Roth Conversion before becoming ROR in India